You might be interested in

4 min to read

AJ Bell’s Russ Mould explains what investors should look for if they want to keep tabs on sentiment surrounding the world’s largest stock market.

Source: Trustnet

Political instability, companies working for the government rather than shareholders and independent bodies being influenced by the head of state. These may all sound like traits of an emerging market but are all currently playing out in the world’s preeminent economy: the US.

This week, president Donald Trump attempted to fire Federal Reserve governor Lisa Cook due to mortgage fraud allegations, although the decision is subject to a legal dispute. Regardless, it brings into question the independent nature of the body.

Meanwhile, his government has taken a 10% stake in Intel, one of the largest American manufacturers of semiconductors, with suggestions that it may not be done adding to the country’s stock portfolio.

Russ Mould, investment director at AJ Bell, said: “Efforts by a political leader to influence central bank policy, interference in the choice of chief executives of leading companies and the sacking of public officials who deliver unwelcome news might not be a surprise in an emerging market, but they are a mighty surprise in America.”

The US stock market, however, has remained unperturbed. The S&P 500 is flat so far this week, while the share price of Intel is only slightly lower than the end of last week, something that surprised Mould.

“Intel’s shares have held up well, even though state-backed stake-building and efforts to browbeat its chief executive are usually signs to investors that a company, or industry, may not be run strictly with the aim of shareholder value creation in mind but to the benefit of a political agenda, in the form of local employment, investment, or both,” he said.

“Investors tend to fight shy of industries where national champions are promoted, as the profit motive tends to get lost in the political wash. Even if a stock, industry or country’s headline index are not entirely spurned, they tend to be afforded lower multiples and valuations to reflect the additional political risk.”

However, there have been movements in other markets that investors may want to use as a bellwether for how people truly feel about the latest developments coming from the White House.

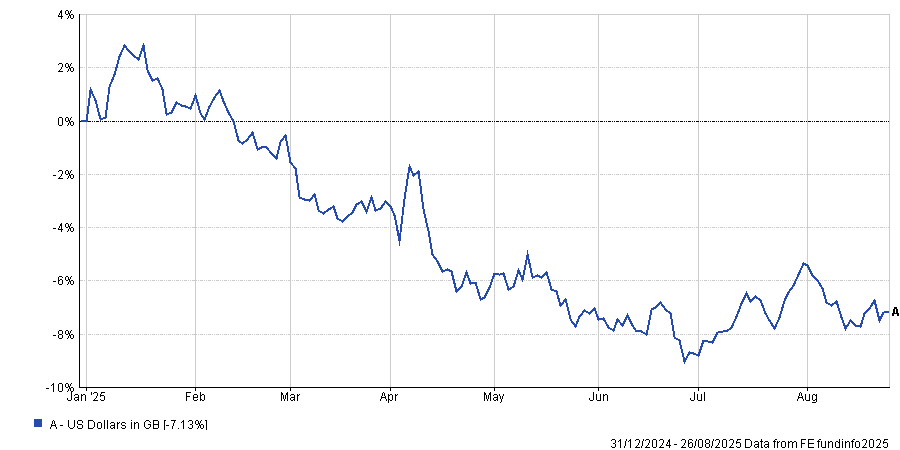

The first is the dollar, which has weakened by around 7.1% against the pound so far this year, as the below chart shows.

Dollar versus pound in 2025

Source: FE Analytics

Any further weakness would “point to increased aversion to US assets”, said Mould, while strength would signify renewed comfort.

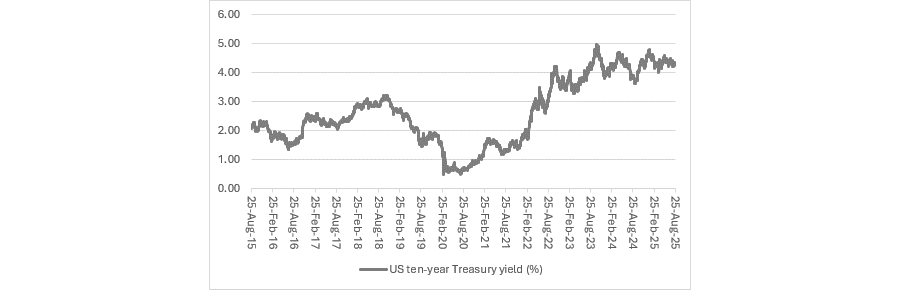

The second is US 10-year treasury yields, which have climbed slightly over the past year, despite calls from the president for the Fed to cut rates (which would in turn bring down treasury yields).

10-year treasury yields over time

Source: FE Analytics

Mould noted Trump’s tax cut-and-spend plans could “raise fresh worries about the galloping US deficit”, even if tariff income from his trade tirade could provide a source of incremental revenue.

“Rising yields would speak of concern, especially if they keep going up as the Federal Reserve cuts interest rates, and falling ones of improved sentiment,” he said.

Last is the trend already underway with overseas equities, such as the UK, Europe, Japan and emerging markets. For the past 15 years the US has been the place to invest, but this is beginning to broaden out. While the US market has not suffered, early signs of others catching up could show an apathy towards American companies.

Mould highlighted the emerging markets in particular, as these “are traditionally a beneficiary of a weaker dollar”, as most of the debt taken on by companies tends to be in the American currency, so a weaker dollar will lower the cost of paying this leverage down in local currency.

“Emerging economies also learned their lesson from their own debt crisis of the late 1990s and, as a rule, carry healthier sovereign balance sheets than the US (and many other Western nations),” he added.

Mould suggested investors could track this through the performance of the MSCI Emerging Markets index, while also noting that the MSCI World ex US benchmark (which is a developed market index without US companies) will also show investor trends.

“If both indices continue to run, then there really may be something afoot. Gains for those indices would not mean the US is about to collapse, just that it may be ready to underperform after a lengthy period of dominance,” he said.

Bank of Scotland Share Dealing Service is operated by Halifax Share Dealing Limited. Halifax Share Dealing Limited. Registered in England and Wales No. 3195646. Registered Office: Trinity Road, Halifax, West Yorkshire HX1 2RG. Authorised and regulated by the Financial Conduct Authority, 12 Endeavour Square, London, E20 1JN under number 183332. A Member of the London Stock Exchange and an HM Revenue & Customs Approved ISA Manager.

The information contained within this website is provided by Allfunds Digital, S.L.U. acting through its business division Digital Look Ltd unless otherwise stated. The information is not intended to be advice or a recommendation to buy, sell or hold any of the shares, companies or investment vehicles mentioned, nor is it information meant to be a research recommendation. This is a solution powered by Allfunds Digital, S.L.U. acting through its business division Digital Look Ltd incorporating their prices, data news, charts, fundamentals and investor tools on this site. Terms and conditions apply. Prices and trades are provided by Allfunds Digital, S.L.U. acting through its business division Digital Look Ltd and are delayed by at least 15 minutes.

Data provided by FE fundinfo. Care has been taken to ensure that the information is correct, but FE fundinfo neither warrants, represents nor guarantees the contents of information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Past performance does not predict future performance, it should not be the main or sole reason for making an investment decision. The value of investments and any income from them can fall as well as rise.

© 2025 Refinitiv, an LSEG business. All rights reserved.